Isolated, Economics Can’t Win

The main players in today’s economy aren’t “rational men” as assumed in classical economics. They are “sociopathic men.” It’s the first and most important lesson.

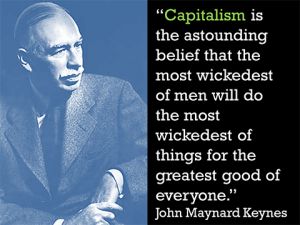

What crippled economics as a science was its separation, in the late 19th century, from other disciplines, especially politics. At the same time, it was decided that economies work because “rational men” (sorry ladies) cause the supply and demand for commodities to balance out at a fair market price.

It’s like the Holy Bible of economics: nobody actually believes it but everybody quotes it.

If we still studied politics and economics together, as we did before economist Alfred Marshall, we would see that it isn’t rationality that makes the world go around, it’s antagonism. Our economy is vastly different from their economy.

Bad Is Good

All these “rational men” do not have identical interests. In fact, our interests are extremely disparate. While ordinary working people like you and me want high employment, good wages, and low prices; our employers usually want the opposite. What is good for us, especially high wages, is bad for them.

Back in Alfred Marshall’s time, this opposition may not have seemed so important to people studying single economic data in a single market. But two great changes have occurred since then that make oppositional understanding vital: world war and governmental economic policy.

National “Good” is International “Bad”

Nations exploit one another. The First World War was fought to determine which industrialized nations were going to do the exploiting. That wasn’t a decision made by rational men within a single economy. “War is politics by other means,” as we say. Politicians made the decisions to carry out world wars, and the winners reaped the benefit. War determined international economics, but it certainly wasn’t because of rational men.

“Whose Economy” Depends on “Whose Government”

Capitalism has a built-in propensity for crisis. Early in the 20th century, and especially during the Great Depression, governments began to take affirmative action to save capitalism from itself. They recognized that monetary policy and fiscal policy could be used to heat up or cool down an economy to some extent.

The biggest problem was oppositional interests. Governments generally interceded in the economy on behalf of the richest capitalists and not for the majority.

But another big problem was created by all this government intervention. Instruments of debt and other purely financial instruments were floating around everywhere, and they became an obsession. A major part of economics was no longer concerned with commodities at all.

Government tried to regulate financial institutions, but they gave that up in 1999 when Texas Senator Phil Gramm got the “Financial Services Modernization Act” passed.

Without regulation, banks and other financial institutions began to use the tremendous resources that they could mobilize in high-stakes gambling. They particularly liked bundles of low-quality mortgage debt and its various crazy derivatives. The bust that followed was called the “Great Recession.” After that, the government re-regulated to some extent, but they are presently disassembling regulations again for the same reason — amazing profits for the very rich.

It’s not in the interest of the people, and it’s not rational. That’s the first lesson.

–Gene Lantz

I’m on KNON radio at 9 AM Central Time every Saturday. Podcasts can be found from the “events” tab on their website. If you are curious about what I really think, check out my personal web site.