The outlook for working families is far worse than usually noted.

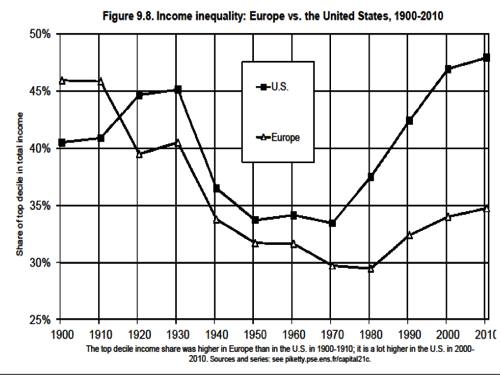

The graph above is one of those used in the best selling, world-shaking economics book “Capital in the 21st Century” by Thomas Piketty.

Like many graphs in the book, this one shows that income inequality dropped during the middle part of the 20th century. Then it began to rise again and continues to rise toward conditions that Monsieur Piketty and others describe as “intolerable.”

Popular economics books of today such as “Runaway Inequality,” a book broadly used in the American labor movement, only look at the later half of the graph – from 1945 to present. Most of the economic analysis used by the AFL-CIO is based on a “return to normal” which they define as 1945-1973. Most of us grew up in that period and consequently it is natural that we would think of it as “normal.”

In 1973, the United States and the world dropped the gold standard and began floating their currencies. After those great economic changes of the Nixon Administration, and even more so under the trickle-down “Reaganomics” of 1980, we say that really bad people distorted American economics to the detriment of working families. Since the bad people took power, inequality has continually grown much worse.

The world owes its gratitude to the Occupy Movement for having focused our attention on rising inequality. They saw that the 1% was growing in wealth and power to the detriment of the 99%, and they forced the rest of us to see it. The unfortunate inadequacy of their solution grew from the shortcomings of their analysis. They didn’t look deeply enough into the data.

Bernie Sanders took this growing consciousness much further. His analysis included the nuts and bolts of inequality, the ways that the 1% keeps the flow of wealth moving upward toward them. Sanders’ prescriptions for new nuts and bolts were much more useful than what the Occupy Movement had offered. Sanders and his followers are converging with the American labor movement today, and both are being strengthened. For that, too, the world must be grateful. I am grateful.

At the same time, during the fiery height of the Bernie Sanders campaign in 2016, even while I was campaigning for him, I often said, “Bernie Sanders will never live to see his program implemented. They would kill him first.”

The solution being put forward by almost everyone in the labor movement and by progressives at large, Bernie Sanders included, is to stop electing bad people and start electing good people who will return to the good policies that reduced inequality during 1914-1973. It’s a simple and seductive solution.

It Won’t Work

I would truly like to think that elections, elections in general and specifically the ones we’re about to have, will elect those good people, with those good solutions, and we will return to the policies that lowered instead of raising inequality in the United States and in the world. But they won’t.

I want to tell you why, even though I supported the Occupy Movement, and even though I support the Bernie Sanders socialists, and even though I am completely devoted to the AFL-CIO and the American labor movement, I want to tell you why I think their analysis is incomplete. Not only is their analysis incomplete, but their prescription, what to do about our situation, is inadequate. One cannot arrive at successful tactics without first understanding the present situation.

Look at the Whole Graph

The popular analysis, and the prescriptions that come from it, are wrong. Look at the whole graph. In fact, look at the entire history of capitalism. Piketty and his associates have accumulated data and anecdotal records going back to the early days of capitalism. Those data show incontrovertibly that increasing inequality is fundamental to capitalism. The 60-year drop in inequality, roughly from World War I until 1973, a small part of capitalism’s history, was never normal. It was completely abnormal and, in fact, antithetical to normal capitalism. What we had before 1914, and what we have now, rising inequality, is “normal.”

Didn’t Work in 2008, Won’t Work in 2018

If one realizes that we are now living in a “normal” period, then one should be able to see that there is no single simple solution. Even if we have great election victories in 2018, as we did in 2008 by the way, inequality is not going to diminish. We’re going to have to work a lot harder than that.

What we are living in now, and what we lived in before World War I, is normal. In an article titled “Who Will Be the Winners of the Crisis?”, Piketty himself explains: “Left to itself, capitalism, because it is profoundly unstable and inegalitarian, leads naturally to catastrophes.” “Inegalitarian” means what you think it does.

So the period of my youth was abnormal. What we are suffering under today is normal.

Why Did Inequality Diminish in the Abnormal Period?

Monsieur Piketty points out that the crises of the 20th century did not cause inequality to go down. As he says in the article I just quoted, “The historical data… shows unambiguously that that financial crises, as such, have no lasting effect on inequality; it all depends on the political response to them.”

So the political responses to the two world wars and to the great depression were what lowered inequality. It was the progressive taxation that lowered inequality. But why did these progressive policies get selected? Why not let the rich continue getting richer and the poor get poorer? Piketty says that the system received “shocks” with two world wars and a great depression.

Look At the Graph Again

Piketty is wrong about the “why” of diminished inequality 1914-1973. It wasn’t “shocks.” It was the success of the working class. We may not know much about the 23 countries that Piketty studied, but we do know what happened in the United States in the middle of the 20th century.

Workers Power Grew

In 1914, when Piketty says inequality began to get lower, the Socialist Party was riding high in America. Even out here, in Texas and in Oklahoma, many people were openly socialists. They voted socialist. There were socialists elected here and there and everywhere. There were socialists in Congress! The Industrial Workers of the World was terrifying employers from the textile mills of New England to the timber forests of Oregon. In 1917, socialists took power in the Russian empire! In 1919, Eugene Debs got a million votes for President while he was in prison!

The great depression hit hard in the capitalist countries, but the socialists were able to point to the Soviet Union and say “They aren’t having a depression!” Socialism, and the workers movement, was growing in popularity while inequality was falling. During World War II, it was the socialists who led the resistance movements. Many of them were so popular that they took power when the Germans and Japanese were finally defeated. Look at Marshall Tito in Yugoslavia, Enver Hoxha in Albania. Look at Mao Tse Tung in China and Ho Chi Minh in Vietnam!

In 1935 in America, the Committee for Industrial Organization took over where the Industrial Workers of the World left off. The progressive movement grew like crazy. By 1947, they had gone from a small part of the labor movement to approximately 1/3 of the American workforce! The actual numbers of people in unions continued to rise until the mid-1950s. Then it started to drop off. In that same period, socialists were red-baited into virtual obscurity. The Soviet Union was probably at the height of its world popularity when it sent up Sputnik in 1957, but its popularity sagged after that. By the time Reagan declared war against the progressive movement, the steam had gone out of the workers’ movement, both internationally and here.

I saw one book, sold by the AFL-CIO, that says the American labor movement died in 1972 because they failed to support McGovern for President. We didn’t actually die, but we lost a lot of blood.

However one may analyze it, no matter what statistics one uses, one still has to conclude that the workers’ movement does not have the power that it enjoyed in the middle of the century, when inequality was at its lowest.

After 1980, the power of American employers waxed while ours waned. Inequality grew. Inequality is still growing.

While Employers Rule, Workers Can Make No Permanent Gains

The greatest person I ever knew personally was named George Meyers. He had been a leader of the CIO before he joined the army in World War II. George used to say, ‘There are no permanent gains for workers under capitalism.” No matter what you win, you will always have to fight for the same things again.

I had a personal experience with that. My union carried out an incredible fight in 1984-5, and we emerged with the best contract in the aerospace industry. Better than Boeing’s contract, and we were just little LTV in Grand Prairie, Texas. But nobody hangs on to those gains. You have to win them over again, the same things, win them over and over and over, every contract.

With Understanding, We Can Prescribe Solutions

The solution to the rising inequality caused today by normal capitalism is to fight with everything we can find. We have to fight to win these elections, of course, and we really need to win. But that’s not all. We need economic struggle as well as political struggle. We need boycotts, we need petitioning campaigns, we need militant contract fights, and above all we need to organize. We need to bring the entire progressive movement together and focus it on fighting the employers, the 1%.

It’s easy to say these things but not so easy to do. Contract fights are rare today, because the legalities have become so rigorous against us and our leaders have lost their edge while our members are confused. Even a simple idea like organizing is really really hard. Most union staffers and officers are far too busy to organize. There’s very little money for organizing, and there are very few unpaid volunteers in today’s labor movement.

But There’s Good News

We are in the biggest and most general progressive upsurge in American history. It isn’t focused, it isn’t united, but it’s big and it’s enthusiastic. The most exciting news of the 21st century came from the teachers of West Virginia and a few other states this year. They carried out victorious political strikes. Political strikes are common in Europe, but almost unheard of in America. That kind of planning, that kind of volunteering, and that kind of militancy is what we have to have.

I won’t say it’s easy to do what has to be done, but I will say that it has to be done. There is no other way.

–Gene Lantz

I’m on KNON radio 89.3FM in Dallas at 9 AM Central time every Saturday. They podcast it on Itunes. If you are curious about what I really think, see my personal web site. I intend to present the ideas in this article at 6:30PM Central Time on September 1 at Romo’s Restaurant, 7033 Greenville Av in Dallas. Come down and discuss it!